To apply for a credit card, check your credit to see what you’ll qualify for, choose a credit card type, compare multiple card options and apply for the best credit card for your goals and spending habits.

At Experian, one of our priorities is consumer credit and finance education. This post may contain links and references to one or more of our partners, but we provide an objective view to help you make the best decisions. For more information, see our Editorial Policy.

You can apply for a credit card by checking your credit to see what you'll qualify for, choosing a credit card type, comparing card options and submitting an application.

Opening a new credit card can be a pathway to building credit and earning rewards on the purchases you regularly make. Before you apply for new credit, learn how to pick the best credit card for your goals and spending habits. It's also key to understand a credit card's terms and fees to ensure you avoid extra charges.

Here's how to apply for a credit card.

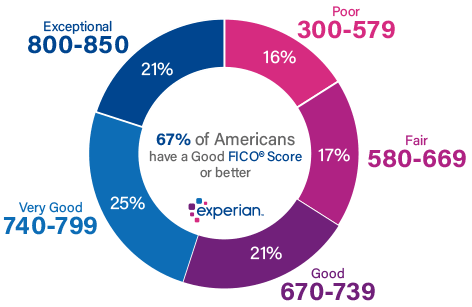

Your credit score typically has the biggest impact on whether you'll get approved for a credit card. It affects not only your odds of qualifying for a specific credit card, but the credit limit and interest rate a lender offers you.

Check your FICO ® Score ☉ for free through Experian to understand which type of cards you'll be eligible for. Scores range from 300 to 850; a higher credit score indicates lower risk and can make it easier to qualify for credit, while a low credit score can limit your options.

Here's a breakdown of the FICO ® Score ranges and how they may impact your ability to qualify for a credit card:

Tip: You generally need good or excellent credit to qualify for cards with the best rewards and benefits.

If you want a credit card that may be difficult to qualify for with your current credit score, take some time to improve your score before applying.

There are several types of credit cards on the market, and the best option for you is the one that matches your current spending habits. Here's what to know about the most common types of credit cards:

| Types of Credit Cards | ||

|---|---|---|

| What It's Best For | Credit Score Requirements | |

| Rewards credit cards | Earning cash back, points or miles on your spending | Good or excellent credit; some issuers offer cards to applicants with fair credit |

| Balance transfer credit cards | Avoiding interest charges while you pay off a credit card balance | Good or excellent credit |

| 0% introductory APR credit cards | Financing a large purchase at 0% interest during the promotional period | Good or excellent credit |

| Student credit cards | Building credit and earning rewards while enrolled at a two- or four-year college | No minimum; some credit history may be required |

| Secured credit cards | Building or rebuilding credit | Generally available to those with poor credit |

| Store credit cards | Earning rewards and discounts at a store where you frequently shop, though other credit card types may be better bets | Generally available to those with fair credit; some issuers may approve applicants with poor credit |

Once you've identified the type of card you'll apply for, compare multiple options to make sure the card you choose has the best benefits and terms available. You can submit a prequalification online to see what cards you're likely to qualify for.

Here's what to look for when comparing a few credit cards that you think could meet your needs:

See your current credit card offers based on your credit profile.

From cash back rewards to a low intro APR, compare your options.

Apply knowing you’re more likely to qualify with matched offers.

Once you've picked a specific card, it's time to get granular and look closely at its terms. These include specific fees and interest rates that can affect the card's cost to you. Most of this information is available in a format called the Schumer Box on a credit card offer or statement.

Next, apply for the credit card you've chosen. You'll need to submit the following information:

Tip: You need to be 18 to apply for a credit card. And if you're under 21, you'll need to show proof of income.

The application process itself is relatively quick online, and you may be approved right away if you meet the issuer's credit requirements. If not, the issuer may take up to a week to review your application.

You may receive a notification that your credit card application is under review. That means the issuer needs more time to decide whether you're approved, and it could be due to missing information on the application, verification of certain data or other reasons. You can contact the issuer to check the status of your application and to offer additional information to aid in the decision-making process.

If you're approved, it can take up to 10 days to receive a credit card in the mail. The issuer might offer the option for expedited shipping, which could come with a fee. Some lenders provide you with a temporary virtual credit card number you can use for online purchases while you wait for your regular credit card to arrive.

Once you get your new credit card in the mail, you must activate your card and online account. Check its credit limit, billing cycle and payment due date, and note that the best way to keep your credit in good shape is to aim to pay off at least the statement balance each month.

The minimum credit score that you'll need for a credit card depends on the type of card and the lender's criteria. Having a good credit score—of 670 or higher—is the best way to ensure you'll have your pick of credit cards, no matter the type. If you're opting for a secured credit card, store card or student card, you'll often be able to qualify with a lower score.

Yes, you can still qualify for a credit card with no credit. Secured cards, student cards and store cards are geared towards applicants with no credit history. These types of cards make a good first credit card and can help you establish credit when you make on-time payments and maintain a low credit utilization.

You will receive an adverse action letter if your application is denied, which will explain the reasons for the rejection. Using that information, you can work on improving your credit and applying again later. Or choose a secured credit card instead to help strengthen your score.

To work toward better credit, make all bill payments on time, keep debt balances low, avoid applying for multiple new types of credit and keep your oldest credit accounts open and active.

There's no specific number of credit cards that you should have. It's ideal to have at least one to use it responsibly and build credit. You have too many credit cards if you have a hard time keeping track of them, you're building up debt you can't repay and the fees are unaffordable.

Applying for a credit card is usually quick. The research required to make sure you've chosen the right one to apply for can be a longer process. Take the time to ensure you're opting for a card that you can confidently manage without accruing substantial interest charges and fees—and that will most benefit you and your credit.

Apply for credit cards confidently with personalized offers based on your credit profile. Get started with your FICO ® Score for free.

Experian's Diversity, Equity and Inclusion

To view important disclosures about the Experian Smart Money™ Digital Checking Account & Debit Card, visit experian.com/legal.

The Experian Smart Money™ Debit Card is issued by Community Federal Savings Bank (CFSB), pursuant to a license from Mastercard International. Banking services provided by CFSB, Member FDIC. Experian is a Program Manager, not a bank.

☉Credit score calculated based on FICO ® Score 8 model. Your lender or insurer may use a different FICO ® Score than FICO ® Score 8, or another type of credit score altogether. Learn more.

Editorial Policy: The information contained in Ask Experian is for educational purposes only and is not legal advice. You should consult your own attorney or seek specific advice from a legal professional regarding any legal issues. Please understand that Experian policies change over time. Posts reflect Experian policy at the time of writing. While maintained for your information, archived posts may not reflect current Experian policy.

Opinions expressed here are author's alone, not those of any bank, credit card issuer or other company, and have not been reviewed, approved or otherwise endorsed by any of these entities, unless sponsorship is explicitly indicated. All information, including rates and fees, are accurate as of the date of publication and are updated as provided by our partners. Some of the offers on this page may not be available through our website.

Offer pros and cons are determined by our editorial team, based on independent research. The banks, lenders, and credit card companies are not responsible for any content posted on this site and do not endorse or guarantee any reviews.

Advertiser Disclosure: The offers that appear on this site are from third party companies ("our partners") from which Experian Consumer Services receives compensation. This compensation may impact how, where, and in what order the products appear on this site. The offers on the site do not represent all available financial services, companies, or products.

*For complete information, see the offer terms and conditions on the issuer or partner's website. Once you click apply you will be directed to the issuer or partner's website where you may review the terms and conditions of the offer before applying. We show a summary, not the full legal terms – and before applying you should understand the full terms of the offer as stated by the issuer or partner itself. While Experian Consumer Services uses reasonable efforts to present the most accurate information, all offer information is presented without warranty.

© 2024 All rights reserved. Experian. Experian and the Experian trademarks used herein are trademarks or registered trademarks of Experian and its affiliates. The use of any other trade name, copyright, or trademark is for identification and reference purposes only and does not imply any association with the copyright or trademark holder of their product or brand. Other product and company names mentioned herein are the property of their respective owners. Licenses and Disclosures.